The Strategic Asset Management Plan is the document that gives an asset management system its strategic direction. It answers the question that governs every asset decision an organisation makes: how will we manage our assets to deliver what the organisation is trying to achieve? The answer, documented and communicated across the organisation, is what makes asset management a coherent system rather than a collection of well-intentioned activities operating in different directions.

ISO 55001 makes this explicit. Clause 4.4 requires every organisation implementing the standard to develop a SAMP that documents the role of the asset management system in supporting achievement of the asset management objectives. Clause 4.1 requires those objectives to be aligned with and consistent with the organisational objectives. The SAMP is where that alignment is established, articulated, and made traceable to everyone responsible for implementing it.

This article explains what the SAMP is, what it must contain to meet both the standard's requirements and the practical needs of a functioning asset management system, and how to build one that serves as a genuine management tool rather than a compliance document.

A Translation Document, Not a Maintenance Plan

The SAMP is the strategic bridge between your organisation's objectives and the way you manage your assets, and understanding this function shapes everything about how you write it.

The GFMAM Asset Management Landscape Third Edition (2024) defines the Asset Management Strategy, contained in the SAMP, as a document that "translates organisational objectives into asset management objectives, defines the organisation's asset management system and the approach to asset management and the organisation's assets, and describes the strategies and actions to deliver on asset management objectives." That definition starts with organisational objectives and works downward.

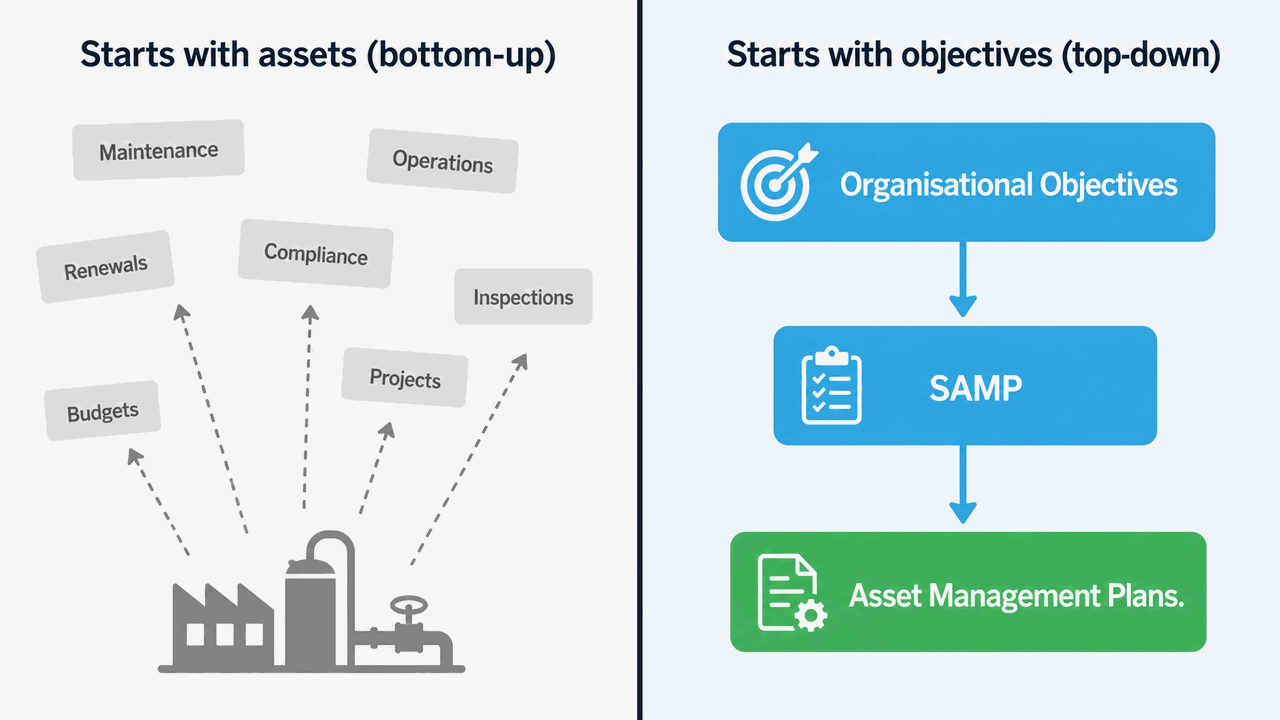

The SAMP does not begin with an asset inventory or a maintenance schedule. It begins with what the organisation is trying to achieve, and then establishes how the asset portfolio will be managed to support that. Maintenance schedules, capital programmes, inspection plans and work orders are important, but they are operational outputs that flow from the SAMP. The SAMP sits above them in the governance hierarchy and provides the strategic context within which they are justified and prioritised.

This distinction matters because the SAMP's primary audience is not the maintenance planner or the site engineer. It is the executive team, the board, and the senior operational and financial leadership who make decisions about capital allocation, risk appetite, and the performance standards the organisation commits to. Those readers need to see their business objectives reflected in the SAMP's purpose and language.

The Governance Hierarchy: What Sits Above and Below the SAMP

The SAMP's influence comes from its position in the governance structure, bridging the strategic commitments made at leadership level and the operational plans executed on the ground.

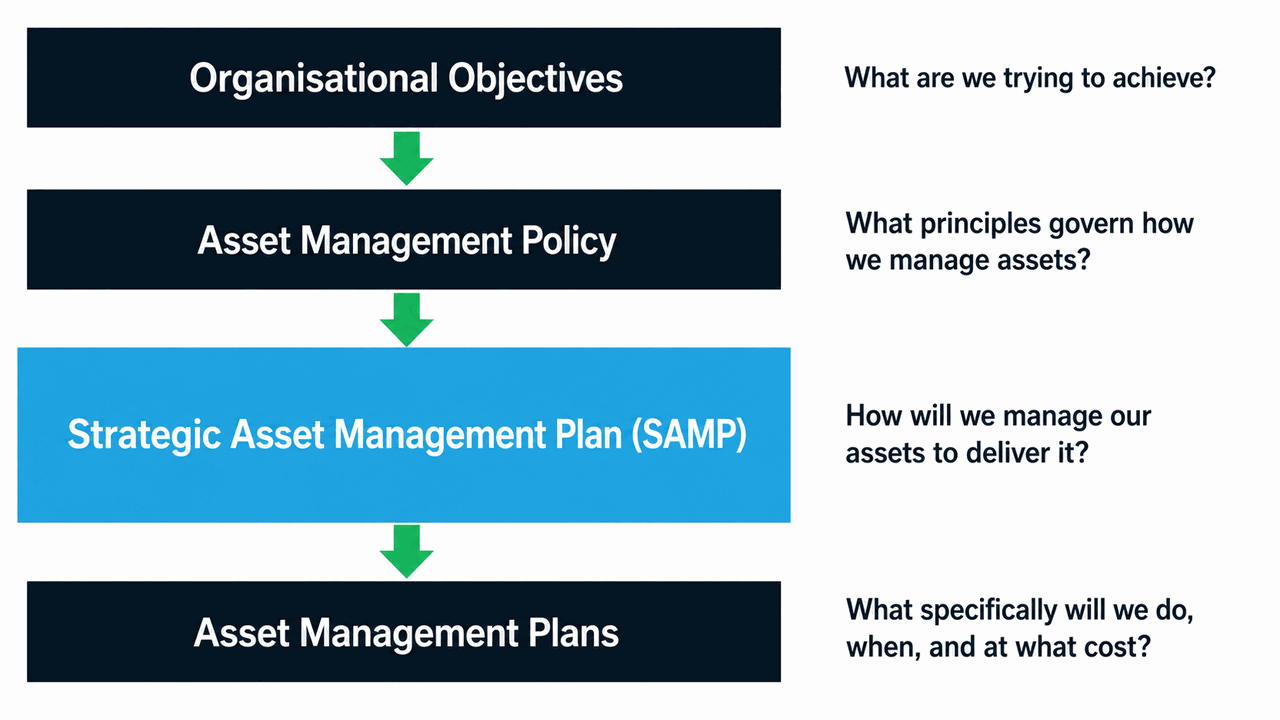

ISO 55001's governance structure follows a clear cascade. At the top sits the organisational plan, which establishes what the organisation is trying to achieve. Below that sits the asset management policy, which commits the organisation to managing assets in a way that supports those objectives and provides the framework within which AM objectives are set. The SAMP then translates the policy's commitments into a strategic direction for the asset management system. And at the level below sit the asset management plans, which specify at the asset or asset group level exactly what will be done, when, by whom, and at what cost.

Each level in this hierarchy answers a different question. The organisational plan answers: what are we trying to achieve as a business? The AM policy answers: what principles and commitments will govern how we manage assets? The SAMP answers: how will we manage our assets, as a whole, to deliver what the business needs? The asset management plans answer: specifically, what will we do for this asset or asset group, in this period, to contribute to that?

ISO 55001 Clause 5.1 makes top management's role in this hierarchy explicit. Top management must ensure that the AM policy, the SAMP, and the AM objectives are established and are compatible with the organisational objectives. This is a leadership responsibility rather than an administrative task, because the SAMP is where the organisation's highest-level commitment to asset management is translated into a practical, implemented direction.

The line of sight that results from this hierarchy is the standard's core purpose: every significant decision about assets, from annual maintenance budgets to 15-year capital renewal plans, can be traced back through the AMP to the SAMP objective it serves, and from there to the organisational objective it supports.

What the SAMP Must Contain

ISO 55001 does not prescribe a fixed structure for the SAMP, but its requirements across Clauses 4 through 6 define clearly what it must address.

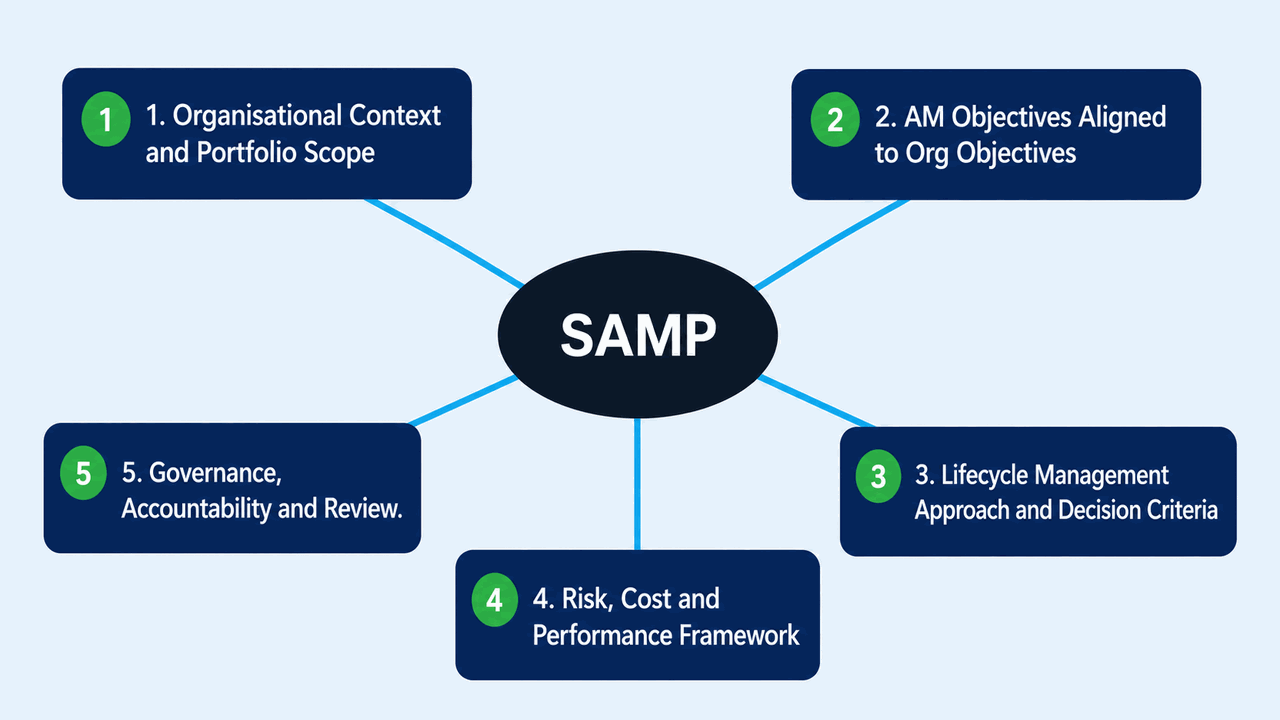

Organisational context and asset portfolio in scope

The SAMP begins with a clear account of the organisation's context: the external and internal factors that shape the environment in which assets are managed. This includes regulatory obligations, ownership structure, stakeholder requirements, market or service delivery conditions, and the nature and scale of the asset portfolio. It defines the boundaries of the asset management system and identifies the portfolio of assets the SAMP governs. This context is not a formality; it is the foundation that makes everything that follows coherent and defensible.

Alignment between AM objectives and organisational objectives

The core purpose of the SAMP is to make the connection between what the organisation is trying to achieve and what it needs from its assets explicit and traceable. AM objectives must be directly traceable to organisational objectives, not loosely associated with them. If the organisation has a regulatory obligation to deliver a defined level of service, the SAMP must establish AM objectives around delivering that service through the performance of the relevant assets. If the board has set a capital efficiency target, the SAMP must establish how the asset portfolio's total cost of ownership will be managed to support it.

Lifecycle management approach and decision-making criteria

The SAMP describes how the organisation will manage its assets from acquisition through to disposal. This includes the lifecycle management methodology it will apply, the criteria it will use for maintenance and capital investment decisions, and the approach to balancing risk, cost and performance across the portfolio. The GFMAM Landscape Third Edition specifies that this includes the methodology for determining asset criticality, which is the analytical foundation on which every prioritisation decision in the asset management system rests.

Risk, cost and performance framework

Every asset management decision involves a trade-off between risk, cost and performance. The SAMP sets the framework within which those trade-offs are made: the organisation's risk appetite for asset failure, the performance standards (levels of service) the asset portfolio must meet, and the TOTEX (Total Expenditure, combining CAPEX and OPEX across the lifecycle) boundaries within which the AM system operates. Without this framework, individual decisions default to departmental precedent rather than a considered organisational position.

Governance, accountability and review

The SAMP assigns accountability for implementing, monitoring and reviewing the AM strategy. ISO 55001 Clause 5.3 requires top management to assign responsibility and authority for establishing and updating the SAMP. The SAMP must identify who owns it, who reviews it, and at what frequency. A SAMP without assigned governance is a document rather than a management tool.

Setting Asset Management Objectives: The Core Strategic Output

Well-constructed AM objectives are the element of the SAMP that determines whether it governs decisions or simply describes them.

ISO 55001 Clause 6.2.1 sets out the requirements for AM objectives. They must be consistent with the AM policy, aligned to the organisational objectives, established and updated using AM decision-making criteria, measurable where practicable, monitored, communicated to relevant stakeholders, and reviewed and updated as appropriate. The standard retains this requirement in the 2024 revision with the same intent.

The practical challenge in writing effective AM objectives is moving from generic statements about asset performance to objectives that are specific, attributable to the asset portfolio's role in delivering business outcomes, and measurable over a defined period. Objectives that connect asset performance directly to business outcomes are the most effective.

An infrastructure operator might set an AM objective around planned availability for the assets that deliver its core service, because availability is the direct mechanism by which commercial obligations are met. A mining operation might express AM objectives in terms of TOTEX for major asset classes as a percentage of RAV (Replacement Asset Value, the cost to replace the entire asset base at current prices), because controlling whole-of-life cost is what enables sustainable unit production cost. A utilities organisation might frame objectives around return on assets (ROA) and the CAPEX/OPEX balance that delivers the regulatory level of service at minimum lifecycle cost. Each of these objectives speaks to both the engineer managing the asset and the CFO reviewing the capital allocation.

The AM objectives sit at the strategic level and cascade into the asset management plans below. Every item in an asset management plan should be traceable to an AM objective in the SAMP. Where that traceability does not exist, the activity either lacks strategic justification or the SAMP's objectives are incomplete.

Want to put this into practice? Download the SAMP template and build line of sight into your own plan.

The Planning Horizon: Thinking Beyond the Budget Cycle

One of the structural differences between a SAMP and an annual budget document is the time horizon over which it plans.

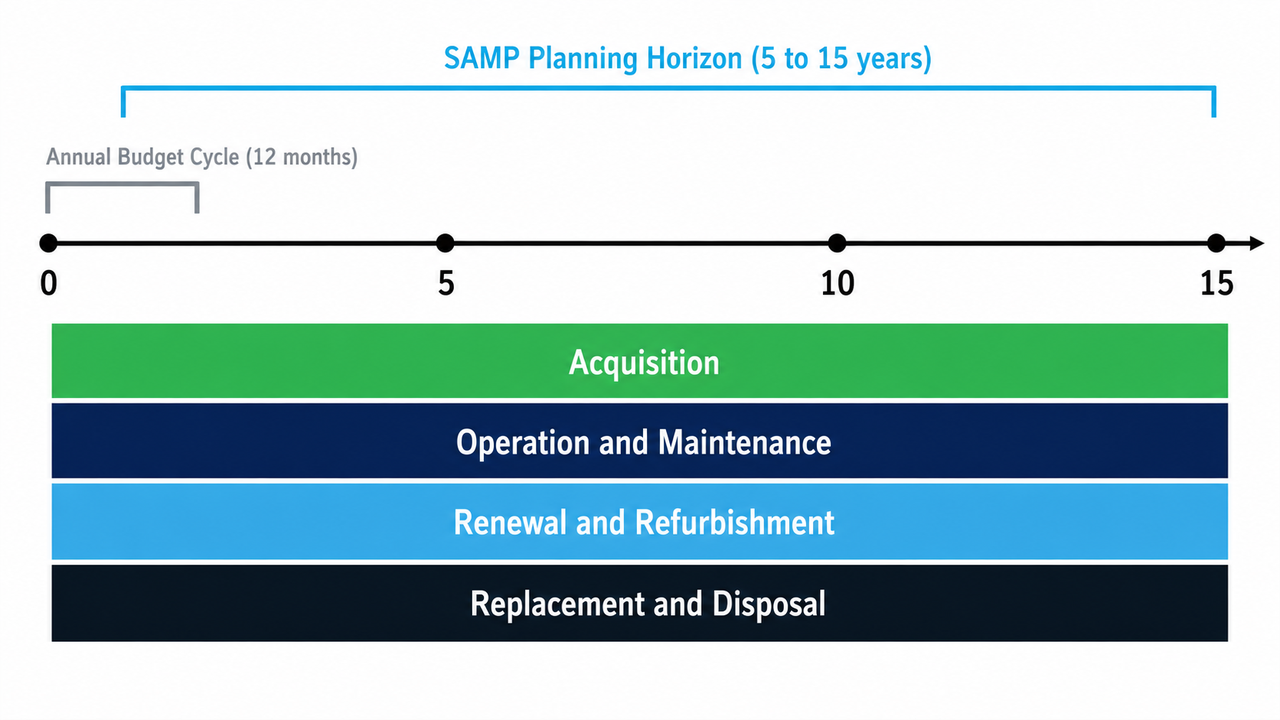

The GFMAM Asset Management Landscape Third Edition states this clearly: "The timeframe for a SAMP typically corresponds to the life cycle of asset portfolios or has a sufficient horizon to accommodate planning for assets, asset management and asset management systems. The planning horizon typically extends beyond an organisation's normal budgetary cycle."

This is a practical and consequential distinction. An annual budget reflects what the organisation can commit to spending in the next 12 months. The SAMP must reflect the reality that asset decisions made today carry cost and performance consequences across years and decades. A decision about whether to undertake a major overhaul or replace a critical item of plant cannot be made well within a single budget cycle. The SAMP provides the strategic context that makes these long-horizon decisions coherent and financially defensible, because the AM objectives and the lifecycle management framework are already established.

A SAMP planning horizon of five to fifteen years is common across heavy asset industries, with the specific horizon driven by the lifecycle profile of the major asset classes in the portfolio. Processing plants with major rotating equipment on 15-year replacement cycles need a SAMP horizon that encompasses that cycle. Transport and infrastructure organisations managing assets with 40-year service lives need a longer strategic view. The SAMP review cadence keeps the document current: annual reviews to check alignment with organisational objectives, and a formal strategic refresh every three to five years. This review period should be stated in the SAMP itself.

The financial planning benefit is significant. A SAMP with a credible long-horizon view provides the basis for lifecycle cost modelling, CAPEX provisioning and OPEX forecasting across the asset portfolio. Organisations that build this into their SAMP find that capital investment proposals are better prepared, because the SAMP provides the strategic context that establishes why the investment is needed and what objective it serves.

Building a SAMP That Governs Real Decisions

A SAMP earns its place in the management system when practitioners can open it and find meaningful guidance for the decisions they face. The following principles apply across industries and asset types.

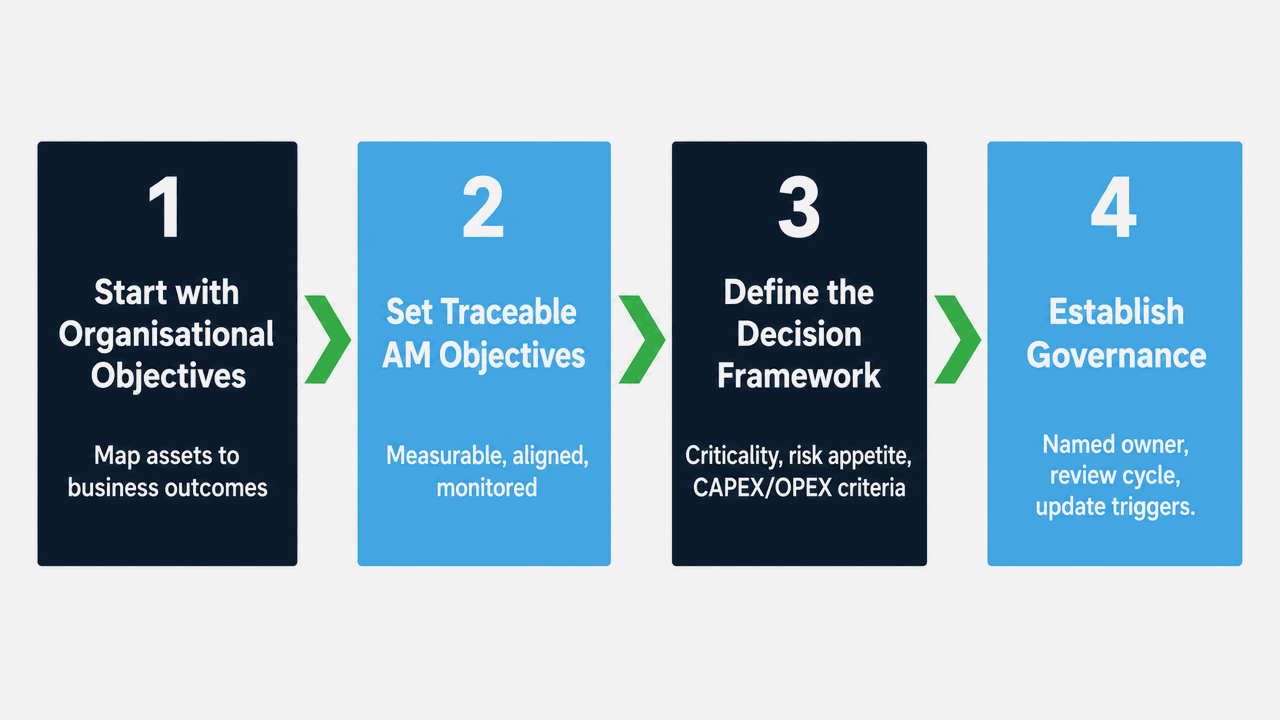

Start with organisational objectives, not the asset inventory

The most reliable path to a SAMP that loses its line of sight is to begin with an asset list and work upward. Begin with the organisational objectives and work downward. For each major objective, identify which asset classes or systems are most critical to delivering it, what level of performance is required, and what the consequence to the organisation would be if that performance was not sustained. This top-down approach produces AM objectives that are genuinely traceable to business outcomes rather than constructed to justify existing practices.

Write objectives that speak to engineers and executives

AM objectives written only in engineering terms create a disconnect from the boardroom. Objectives stated in terms of production availability, total cost of ownership, return on assets, and levels of service connect to the financial and governance conversations that determine how resources are allocated. A well-written SAMP is a document that a board member can read and understand, and an asset engineer can use as a daily reference for prioritisation decisions.

Define the decision framework, not just the decisions

The most durable part of any SAMP is not its specific objectives, which will evolve as the organisation's context changes, but the framework it establishes for making AM decisions. This framework includes the criteria for prioritising maintenance investment, the criticality methodology, the threshold for capital renewal versus major overhaul, and the organisation's risk appetite for different categories of asset failure. When the organisational objectives change, the decision framework helps orient the SAMP quickly in the new direction, because the underlying method for making decisions does not need to be rebuilt from scratch.

Assign governance and set a review cadence

A SAMP is a living document. Assigning a named owner, defining a review trigger (annual minimum, plus a review whenever the organisational objectives change materially), and establishing a clear process for approving updates are not administrative details. They are what make the difference between a SAMP that stays current and one that drifts out of alignment with the organisation it is supposed to serve. ISO 55001 Clause 9.1 requires monitoring and review of the AM system; the SAMP's governance cadence is the mechanism by which that review produces documented, accountable outcomes.

The Document That Makes the System Coherent

The Strategic Asset Management Plan is the document that gives an asset management system its coherence. It closes the gap between the commitments made in the AM policy and the work specified in the asset management plans. It gives engineers, asset managers, maintenance planners and capital project teams a shared strategic reference point for the decisions they make every day.

The organisations that build effective SAMPs treat the document as a management tool. They start with the organisational objectives, build AM objectives that are directly traceable to those objectives, set a decision-making framework that provides consistent guidance across the portfolio, and maintain the governance cadence that keeps the SAMP current. The result is an asset portfolio managed in deliberate pursuit of what the organisation is actually trying to achieve, at a cost and risk level the organisation has consciously decided to accept.

That is the line of sight that ISO 55001 requires, and that a well-built SAMP delivers.